If you still haven't downloaded my "Safe Trade Options Formula" book... ...please take a few seconds and download it right now before your new temporary download link expires. I eventually plan to charge for this book, so do yourself a favor and download it now... That way, no matter how much it is in the future, you'll have a copy on your computer already. Make sense? FREE: Safe Trade Options Formula << Download Now Good Trading,

Bill Poulos p.s. Go here to save a copy of my "Safe Trade Options Formula" book to your computer before I start charging for it.

More Reading from MarketBeat.com

5 Ways to Play Prime Day That Aren’t AmazonAuthored by Thomas Hughes. Published: 6/23/2026.

Key Points

- Amazon is best-positioned to benefit from Prime Day, which is expected to generate a 9% sales increase with Amazon holding a 60% eCommerce share during the event.

- Retailers Walmart and Target are running competing sales events to defend and capture market share from Amazon during the Prime Day window.

- Payment processors Visa and MasterCard, along with buy-now-pay-later provider Affirm, stand to gain indirectly as Prime Day drives a surge in consumer spending.

- Special Report: The #1 stock to buy AFTER the June 12th filing

Amazon (NASDAQ: AMZN) is the prime stock for investors looking to play Prime Day, as it is the event’s originator and central hub. This year’s event runs June 23–26, 2026—a four-day, 96-hour window that Amazon has moved up from its usual July slot. Key details for investors to watch this year include the expected 9% increase in period sales, Amazon’s 60% share of e-commerce during the event, and its influence on consumer habits. Studies have shown that consumers strategically wait to stock up on low-cost essentials, setting the stage for some vendors to outperform others.

However, while Amazon is best positioned, it is not the only company that stands to benefit. #1: Walmart Fights Back to Defend Market ShareWalmart (NASDAQ: WMT) is a good play on Prime Day, too, because it is the world’s largest retailer with a growing, robust online presence. It leans heavily into weeklong sales events intended to defend market share, and they work. Walmart times its sales events to start earlier and last longer than Prime Day, with an omnichannel presence and broad accessibility. This setup allows shoppers to take advantage of same-day delivery and in-store pickup deals without needing an Amazon Prime subscription. Outside of its sales events timed to coincide with Prime Day, WMT catalysts include expectations that earnings growth will accelerate over the course of the year. Quarterly growth is expected to top 9% year over year in the current quarter, then accelerate modestly each quarter for several quarters thereafter. Analyst trends are positive, with sentiment firming and price target revisions moving well above the existing high.

#2: Affirm Captures Market Share With Buy-Now-Pay-Later OptionsAffirm (NASDAQ: AFRM) is a strategic play on Prime Day because it enables shoppers to buy higher-ticket items with a lower upfront cost. With as much as 10% of Prime Day business expected to fall into the buy-now-pay-later category, Affirm is expected to see a seasonal boost and sustain its high-double-digit growth pace. More importantly, the company will significantly expand its loan portfolio, increase recurring revenue, and improve its long-term outlook. As it stands, Affirm is forecast to sustain a solid double-digit growth rate over the next five to six years and widen its margin along the way. Twenty-nine analysts rate Affirm stock a Moderate Buy by consensus, with recent revisions in the high end of the range, forecasting fresh highs by year’s end. They cite the company’s strong underwriting standards, the push for a bank charter, and ecosystem scalability as growth drivers.

#3: Visa Cashes In as the Network Behind the CardsVisa (NYSE: V) is uniquely positioned to benefit from Prime Day as the world’s premier payment processing platform. Details are sketchy, but Visa and competitor MasterCard are believed to handle upwards of 90% of global volume, with Visa accounting for as much as 60% in the core U.S. market. Not only is it the force behind most major cards, but it also has partnerships with Amazon, reflected in the Amazon-branded Visa Prime card. It enables cash back, bonuses, and other incentives that boost business, membership, and loyalty for both the merchant and the processor.

#4: Mastercard Rounds Out the Payment Processing PlayMasterCard (NYSE: MA) is a great play on Prime Day, as it commands the remaining market share not captured by Visa. In this scenario, there is likely to be a modest spike in revenue and earnings, alongside organic growth drivers and a strengthening outlook for capital returns. MasterCard pays a token dividend, worth approximately 0.7% as of mid-2026, and aggressively buys back shares. Q1 activity helped reduce the count by approximately 2.3% year over year (YOY), a pace expected to continue in upcoming quarters. Twenty-eight analysts rate MA stock as a consensus Buy with 35% upside, and institutions have been accumulating aggressively, running at a pace of approximately $3 to $1 on a trailing 12-month basis.

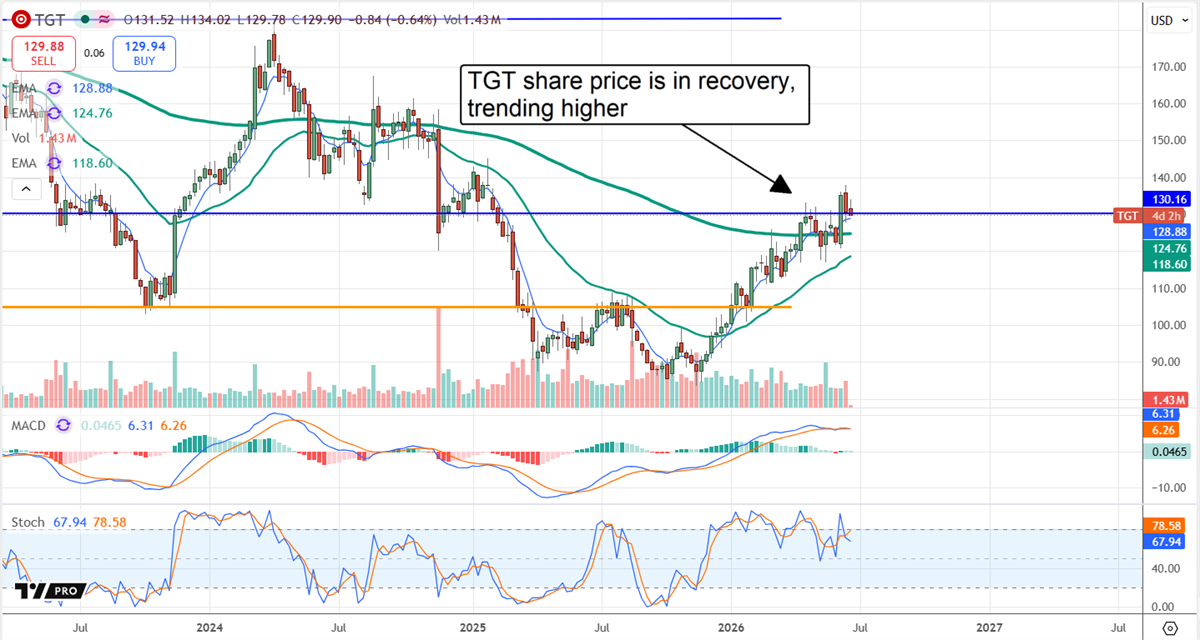

#5: Target Aims to Capture Amazon’s BusinessTarget (NYSE: TGT) is another retailer actively working to retain its share and potentially capture additional share during Prime Day. It relies on the fact that many shoppers compare deals across platforms, using the opportunity to convert traffic with its own deals. Because it focuses on daily items and essentials, it also converts a high rate of impulse purchases. The takeaway for TGT investors is that it offers a lower-cost entry point compared with WMT and attractive capital returns. The dividend yields more than 3.5%, while share buybacks incrementally reduce the share count. Target’s catalysts this year include business recovery. The company is still in the early stages of recovery but showed some traction in its last report, with comps up nearly 4.5%, which has its price trending higher in late Q2 2026. The likely outcome is that it continues to build momentum in subsequent quarters, improving both its revenue and earnings quality. Thirty-three analysts rate Target as a consensus Hold, but sentiment has been firming, and price targets are improving ahead of the expected mid-August earnings release.

. |

0 Comments:

Post a Comment

<< Home