Key Points

- Oil and gas companies benefit from rising crude prices, but so do wholesale club retailers like Costco and BJ's.

- Wholesale clubs offer discounted gas, which entice membership sign-ups and increase foot traffic in stores.

- Both COST and BJ stocks look attractive at the moment due to this catalyst, but your preference between the two likely depends on your risk tolerance.

- Special Report: Elon Warns of Impending "Chip Wall." His Solution Inside.

For many in the United States, high gas prices are the most visible reminder of the ongoing conflict in Iran. And with Brent crude prices now topping $115 as the 2026 calendar flips to April, it appears elevated fuel costs will be with American consumers and businesses through the summer. For the oil and gas industry, high crude prices are welcome news; for everyone else, not so much. Well, there might be one small niche of stock that appreciates high gas prices—wholesale membership clubs.

The Membership Mantra: Gas as a Loss Leader Fuels Warehouse Sales

When gas prices rise, it’s not necessarily a boon to independent gas stations. Oil companies in the energy sector benefit because they can pass on price increases to customers, but gas station operators still pay for refined products at the end of the supply chain, plus taxes and marketing costs. However, for membership clubs like Costco Wholesale Corp. (NASDAQ: COST) and BJ’s Wholesale Club Holdings Inc. (NYSE: BJ), a gas price surge is a unique opportunity, even if the profits don’t necessarily come from fuel pumps.

Clubs like Costco and BJ’s use gas as a “loss leader” to attract new customers and get more foot traffic into their stores. These firms typically sell gas about 10 cents below typical street prices (sometimes as low as 20 to 30 cents), which is possible because of the scale of their operations. Unlike independent stations, Costco and BJ’s negotiate more favorable fuel contracts thanks to their vast networks of stations, which help maintain margins even though they sell at discount prices.

Why sell gas at a razor-thin margin? Because that helps get people in the door, and justifies the cost of their membership. Customers who notice the savings they receive on gas are more likely to venture into the warehouse for higher-margin goods, especially when economic sentiment is poor, and consumers are worried about stretching their dollars. Each company mentions fuel as a membership-acquisition tool in their earnings reports, both as a renewal incentive and to attract new signups.

Costco: Warehouse Club Leader Shows Strength with Retention Rates and Stock Upswing

It's been 18 months since Costco raised its membership rates from $60 to $65 for the basic Gold Star plan and from $120 to $130 for the premium Executive plan, and customers seem to have accepted the increase without much pushback. The company reported a 92% renewal rate during its Q2 2026 results, reported on March 6, along with another impressive comp sales figure of 7.4%. The $69.6 billion in quarterly revenue also represented 9.2% year-over-year (YOY) growth, which handily beat analysts’ projections. Valuation remains the primary concern for Costco investors. The stock trades at more than 54 times forward earnings and 15 times book value, which is a pricey proposition for a retailer with profit margins under 3%.

COST shares kicked off 2026 with 12 gains in 14 trading days, sending the price up 15%. But now a consolidation pattern has enveloped the stock, and shares have bounced between $950 and $1000 for much of the last month. However, the Relative Strength Index (RSI) is about to press above 50, which is generally the level considered necessary for a bullish uptrend. A recent Golden Cross confirms the underlying momentum, and support could now be forming at the 50-day moving average. The stock also secured a recent upgrade to Buy from Weiss Ratings, bringing the consensus to Moderate Buy with an average price target of $1039 (upside of approximately 5%).

BJ’s Wholesale: Undervalued Competitor Quickly Growing Market Share

BJ’s is the smaller, leaner competitor to Costco and Walmart Inc. (NASDAQ: WMT) subsidiary Sam’s Club, but its valuation offers a more attractive investment to risk-conscious investors.

BJ’s operates 263 locations (199 with gas) and recently entered its 21st state with a new store in Kentucky.

Fiscal 2025 was a terrific year for BJ’s; the company opened 14 new stores, the most ever in a single year, and had a tenured membership renewal rate over 90%.

BJ’s also closed the year with an annual record adjusted EPS of $4.40, and its Q4 2025 earnings soared past analyst expectations.

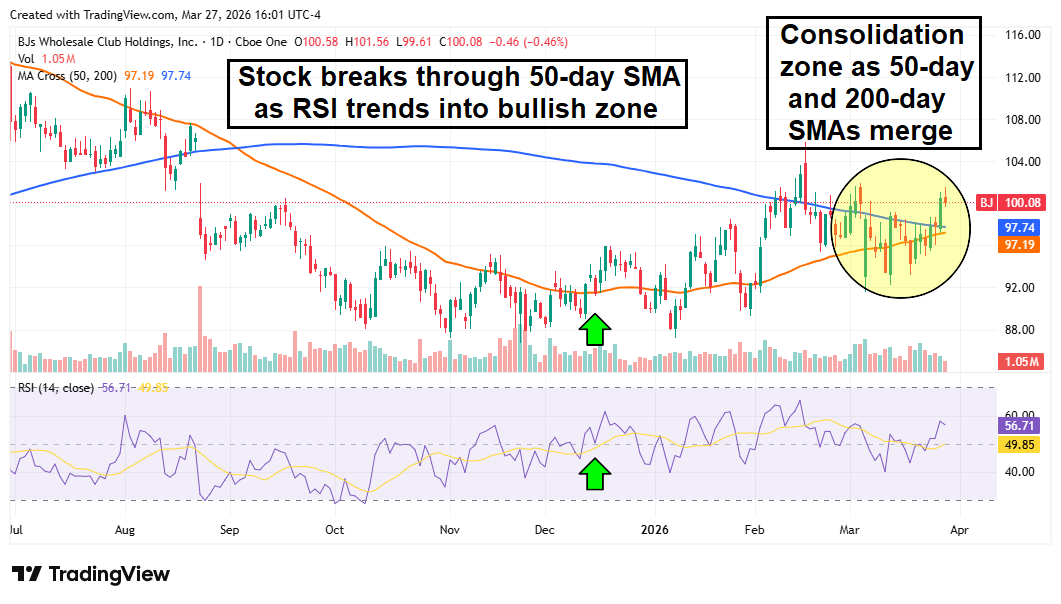

One area where BJ’s shines above Costco is valuation; the stock trades at just 24 times forward earnings despite consistent earnings beats and a growing membership base. Investors looking to open new positions also may be catching BJ’s shares at the start of an upswing. The stock’s prolonged drawdown ended last October, and bullish momentum has been building ever since. The share price retook the 50-day moving average by December and continued trending upward with confirmation on the RSI. The momentum reversal has the 50-day and 200-day moving averages on course for a Golden Cross, which could trigger the next wave of buying pressure.

Read this article online ›

The best investment opportunities don't wait. Get our research and stock ideas delivered straight to your smartphone—so you never miss a market-moving opportunity. Our text alerts ensure you see timely stock ideas and professional research reports instantly, whether you're in a meeting, commuting, or away from your desk.

Get Text Alerts from American Market News (free)

0 Comments:

Post a Comment

<< Home